8/6/2019 Satyam Presentation

http://slidepdf.com/reader/full/satyam-presentation 1/21

1

A Research paper presentation on

́A study of Corporate Governance with specialreference to Satyam Accounting Scandalµ

By

Ms. Muneza Kagzi(MBA Finance-Gold Medalist)-Assistant Professor)

The Mandvi Education Society Institute of Business Management and

Computer Studies

Mandvi, Dist. Surat

Dr. Tripat Kaur (MBA, Ph.d- Director)Shree R.R. Tanti Institute of Management

Ankleshwar

8/6/2019 Satyam Presentation

http://slidepdf.com/reader/full/satyam-presentation 2/21

2

Outline of Research Paper

Abstract Discussion Section 1

-Objectives of the Study

-About the Satyam Company

-Concept of Corporate Governance

-Research Methodology

Section 2

-How the scandal happened actually?-Who are the responsible for the scandal?

Section 3 -Impact of the scandal

8/6/2019 Satyam Presentation

http://slidepdf.com/reader/full/satyam-presentation 3/21

3

Section 1 Objectives of the Study

-To know how the Satyam Scandal happened actually

-To analyze the importance of corporate Governancepractices in context of Satyam Scandal

About the Satyam Company

-In 1987, B. Ramalinga Raju formed Satyam

-Fourth largest Indian IT Company

-In 2008, the World Council of Corporate Governanceawarded Satyam with ³GOLDEN PEACOCK AWARD´ for

global excellence in corporate accountability.-In 2007, Earnst and Young awarded Mr. Ramalinga Raju withEntrepreneur of the Year Award

8/6/2019 Satyam Presentation

http://slidepdf.com/reader/full/satyam-presentation 4/21

4

Section1 Continued«. About corporate Governance

-It¶s a legal and factual framework of the management andmonitoring of companies geared towards transparency to strengthenthe trust in management and control focusing on value creation.

Research Methodology

-Data CollectionSecondary data are used from news paper, various journals andwebsites to carry out this research.

-Time Duration

For the paired sample t test the security prices of before two months of

Satyam Scandal and after two months of Satyam fromwww.nseindia.com

Before two months- 06/11/2008 to 6/01/2009 After two months- 07/01/2009 to 06/03/2009

8/6/2019 Satyam Presentation

http://slidepdf.com/reader/full/satyam-presentation 5/21

5

Research Methodology Continued

- Statistical test usedPaired sample- t test is a statistical technique that is used to comparetwo means in the case of two samples that are correlated. Pairedsample t-test is used in µbefore after¶ studies.

Hypothesis Testing (Paired sample t test)

Null Hypothesis H0

There is no change in the mean return of the Satyam Security beforeand after the scandal

Alternative Hypothesis H1

There is a change in the mean return of the Satyam Security beforeand after the scandal

8/6/2019 Satyam Presentation

http://slidepdf.com/reader/full/satyam-presentation 6/21

6

SECTION-2

1.How the Satyam Scam Occurred?

2.Who are the responsible parties?

On 7Jan,2009 Mr. Raju disclosed in letter to SatyamBoard of director and to SEBI regarding the manipulatingthe accounting numbers for several years.

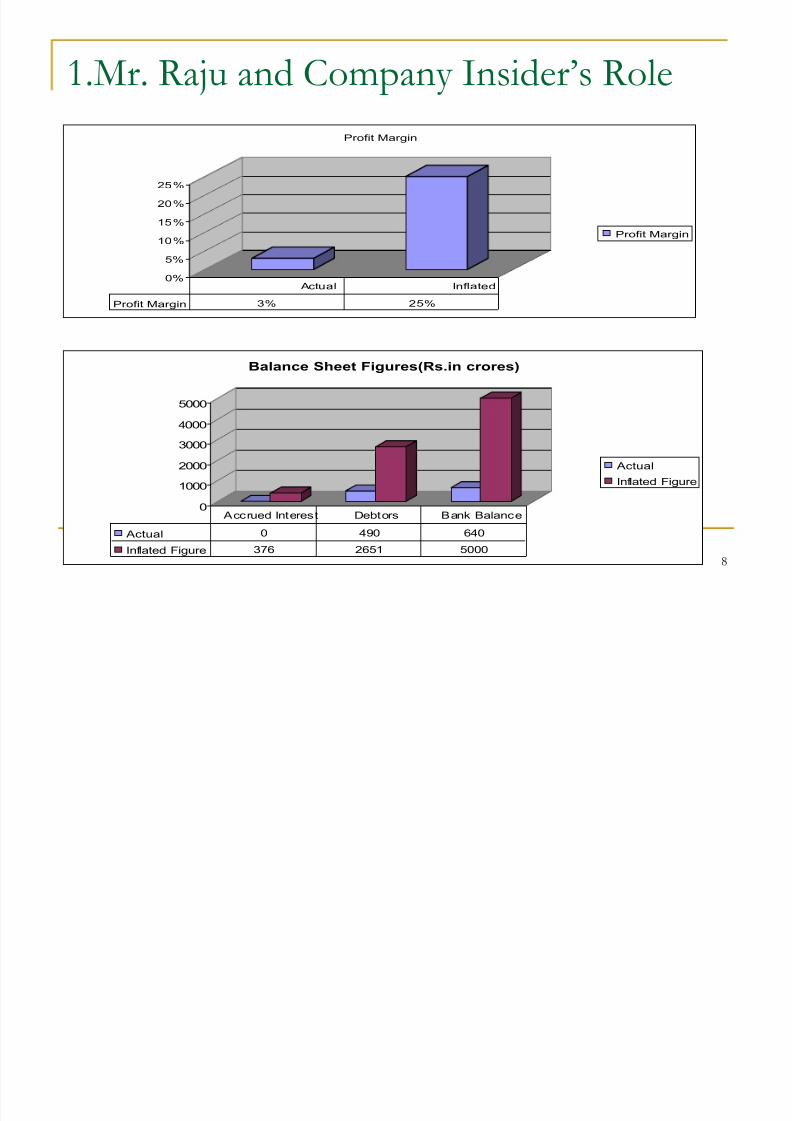

-He has overstated the past seven year¶s account byfraudulently showing a profit margin of about 25% whenin actual it was 3%-An accrued interest of Rs.376 crore which was notexisted.

-An overstated debtor¶s position of Rs.490 core asagainst Rs.2,651 crore in the books.-The cash at hand means in the bank accounts to beRs.5000 crores about a billion dollar whereas the cashwas only Rs.640 crore.

8/6/2019 Satyam Presentation

http://slidepdf.com/reader/full/satyam-presentation 7/21

7

Who are the responsible parties?

From the confession of Mr. Raju he was theprimary responsible person for the fraud

Mr. Raju and Company Insider¶s Role Auditors Role

Board of Director¶s Role

Indian Business and Board Structure

8/6/2019 Satyam Presentation

http://slidepdf.com/reader/full/satyam-presentation 8/21

8

1.Mr. Raju and Company Insider·s Role

0%

5%

10%

15%

20%

25%

Profit Margin

Profit Margin

Profit Margin 3% 25%

Actual Inflated

0

1000

2000

3000

4000

5000

Balance Sheet Figures(Rs.in crores)

Actual

Inflated Figure

Actual 0 490 640

Inflated Figure 376 2651 5000

Accrued Interest Debtors Bank Balance

8/6/2019 Satyam Presentation

http://slidepdf.com/reader/full/satyam-presentation 9/21

9

1.Mr. Raju and Company Insider·s

Role«.-

Continued Using his personal computer, Mr. Raju created numerous

bank statements to advance the fraud. Mr. Raju alsofalsified the bank accounts to inflate the balance sheetwith balances that did not exist

He created 6,000 fake salary accounts over the past fewyears and appropriated the money after the companydeposited it.

Diversion of money to his personal accounts and that thecompany was not as profitable as it had reported;

however, during later interrogations, he had diverted alarge amount of cash to other firms that he owned andthat he had been doing this since 2004.

8/6/2019 Satyam Presentation

http://slidepdf.com/reader/full/satyam-presentation 10/21

10

2.Auditors Role

Global auditing firm Price Waterhouse Coopers ("PWC") auditedSatyam's books from June 2000 for nearly 9 years and did notuncover the fraud, whereas Merrill Lynch discovered the fraud as

part of its due diligence in merely 10 days. PWC signed Satyam's financial statements and was responsible for

the numbers under Indian law. One particularly troubling itemconcerned the $1.04 billion that Satyam claimed to have on itsbalance sheet non interest bearing securities.

It appears that the auditors did not independently verify with thebanks in which Satyam claimed to have deposits.

The fraud went on for a number of years and involved both the

manipulation of balance sheets and income statements. Whenever Satyam needed more income to meet analyst estimates, it simplycreated fictitious sources and it did so numerous times without theauditors ever discovering the fraud.

8/6/2019 Satyam Presentation

http://slidepdf.com/reader/full/satyam-presentation 11/21

11

3.Board of Director·s Role Satyam's Board of Directors consisted of nine members. Members of the Board included Krishna Palepu who is a

Harvard Professor and corporate governance expert,Rommohan Rao, the Dean of the Indian School of Business, and Vinod Dham, co-inventor of the PentiumProcessor.

Satyam revealed that it did not have a financial expert onthe board during 2008. The Board of Directors were having lack of

independence. The Board first came under fire on December 16, 2008

when it approved Satyam's purchase of real estatecompanies in which Mr. Raju owned a large stake. Furthermore, the Board should have caught some of the

same red flags that the auditor, PWC, missed.

8/6/2019 Satyam Presentation

http://slidepdf.com/reader/full/satyam-presentation 12/21

12

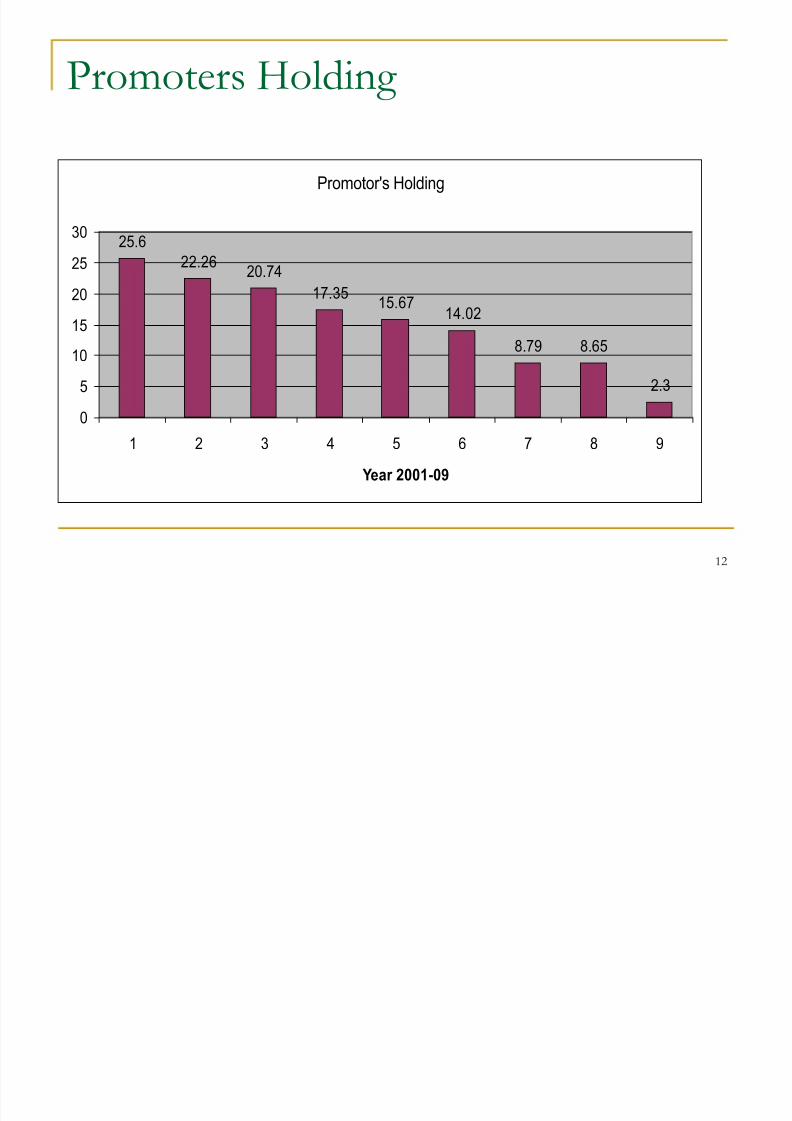

Promoters Holding

Promotor's Holding

25.6

22.26

20.7417.35

15.6714.02

8.79 8.65

2.3

0

5

10

15

20

25

30

1 2 3 4 5 6 7 8 9

Year 2001-09

8/6/2019 Satyam Presentation

http://slidepdf.com/reader/full/satyam-presentation 13/21

13

4.Indian Business and Board Structure

Pervasiveness of family-owned businesses, business promotershave often structured businesses within a pyramid structure whichinvolves owning several different business lines and treating thedifferent businesses as one entity and transferring funds from oneentity to another as needed.

A control group will own 51 percent of the company at the top of the

structure in next tier 26 percent (51 percent of 51 percent) and itsfinancial stake in the third tier is only 13 percent.

The pyramid structure permits groups to control more of theoperations than their equity claims represent.

Consolidated control also makes it more difficult for board membersto be independent from the controlling shareholder

8/6/2019 Satyam Presentation

http://slidepdf.com/reader/full/satyam-presentation 14/21

14

Section 3-Impact of the scandal

Impact on Investors- As on the 7th Jan,2009 the announcement was there of the Satyam

scandal the stock prices reduces from 40.25 to Rs. 23.75 within aday, which shows the erosion the stock prices.

-The t test statistics =-0.445467 which accept the alternative hypothesis

H1 that the mean return has been changed due to scandal.(5%level)

Impact of Satyam scandal on Indian Industry

-The reputation of the company is at the lowest ebb andcontinuation of such a state would affect the confidence in theconcept of corporate governance practiced in India.

8/6/2019 Satyam Presentation

http://slidepdf.com/reader/full/satyam-presentation 15/21

15

B) Regulatory Reform and the

Importance of Corporate Governance1. Governance Reform ± Independent Directors

-Updatation of Corporate Act 1956

-The SEBI is considering several proposals ranging from mandating

increased due diligence on transactions to increasing personalliability of board members.

-SEBI revised takeover regulations to increase disclosure in takeovers.

2. Disclosure of Pledged Securities

-Two weeks after Satyam's collapse, the SEBI made it mandatory for controlling shareholders to disclose any share pledges.

8/6/2019 Satyam Presentation

http://slidepdf.com/reader/full/satyam-presentation 16/21

16

B) Regulatory Reform and the

Importance of Corporate Governance3. Increased Financial Accounting Disclosures

-The SEBI also recently proposed requiring companiesto disclose their balance sheet positions twice a

year.-The increased reporting of companies' balance sheetswill provide investors with more information on thestability of a company's financial position.

- Increasing both the frequency and detail of disclosurewill help provide for a more robust market check²e.g. investors will be able to pay more attention toaccounting irregularities.

8/6/2019 Satyam Presentation

http://slidepdf.com/reader/full/satyam-presentation 17/21

17

B) Regulatory Reform and the

Importance of Corporate Governance4.IFRS (Adoption of International Standards)

-Satyam strengthened India's commitment to adopt InternationalFinancial Reporting Standards ("IFRS") by 2011

-Adopting IFRS will facilitate investor comparisons of financial

performance across country lines and will increase confidence in theaccounting numbers.

5 Creation of New Corporate Code - Ministry of CorporateAffairs

-The Ministry of Corporate Affairs recently proposed a new law to

provide investors with a claim similar to the shareholder derivativesuit that U.S. law permits which would make it easier for Indianinvestors to form class action lawsuits against fraudulent actors inthe company.

8/6/2019 Satyam Presentation

http://slidepdf.com/reader/full/satyam-presentation 18/21

18

Conclusion

As the Satyam Scandal laid down the pillar whichinsists all the corporate to pay attention towards thecareful implementation of Corporate Governance Aswe had seen in this study that in spite of there being a

strong corporate governance framework and stronglegislation in India, top management sometimesviolates governance norms either to favor familymembers or because of jealousy among siblings. Thisshows the lack of regulatory supervision andinefficiency in prosecuting violators.

8/6/2019 Satyam Presentation

http://slidepdf.com/reader/full/satyam-presentation 19/21

19

References

Research Paper (2010) UICIFD Briefing Paper No. 8: India's Satyam

Accounting Scandal by David Winkler-http://www.uiowa.edu/ifdebook/briefings/docs/satyam.shtml

Websites (2007). India stock market hits new high. BBC, Retrieved from

http://news.bbc.co.uk/2/hi/south_asia/7035443.stm (2009). ICIA finds ex Satyam CFO, Price Waterhouse auditors

guilty. Outlook India.com, Retrieved fromhttp://news.outlookindia.com/item.aspx?666905

(2009). India index: [Web]. Retrieved from

http://www.marketwatch.com/investing/index/BSESN/charts?countryCode=xx

(2009). India's Enron. The Economist, Retrieved fromhttp://www.economist.com/businessfinance/displaystory.cfm?story_id=E1_TNJDPQNQ&source=login_payBarrier

8/6/2019 Satyam Presentation

http://slidepdf.com/reader/full/satyam-presentation 20/21

20

References Continued«.

(2009). Satyam fraud is not a system failure: ved jain. Outlook India.com,ttp://news.outlookindia.com/item.aspx?652667

(2009). Text of Mr, Ramalinga Raju's statement.

Business Line, Retrieved fromhttp://www.thehindubusinessline.com/businessline/blnus/05071265.htm

Pricewaterhouse Coopers, (2009). Moving forward:global acceptance of IFRS. Bangkok Post,

Retrieved fromhttp://www.bangkokpost.com/business/economics/27159/moving-forward-global-acceptance-of-ifrs

8/6/2019 Satyam Presentation

http://slidepdf.com/reader/full/satyam-presentation 21/21

21

Thank you«««.

Recommended