Embed Size (px)

Citation preview

Earnings Results 3Q16November, 2016

Disclaimer

This presentation may contain certain forward-looking projections and trends that neither

represent realized financial results nor historical information.

These forward-looking projections and trends are subject to risk and uncertainty, and

future results may differ materially from the projections. Many of these risks and

uncertainties are related to factors that are beyond CCR’s ability to control or to estimate,

such as market conditions, currency swings, the behavior of other market participants, the

2

such as market conditions, currency swings, the behavior of other market participants, the

actions of regulatory agencies, the ability of the company to continue to obtain financing,

changes in the political and social context in which CCR operates or economic trends or

conditions, including changes in the rate of inflation and changes in consumer confidence

on a global, national or regional scale.

Readers are advised not to fully trust these projections and trends. CCR is not obliged to

publish any revision of these projections and trends that should reflect new events or

circumstances after the realization of this presentation.

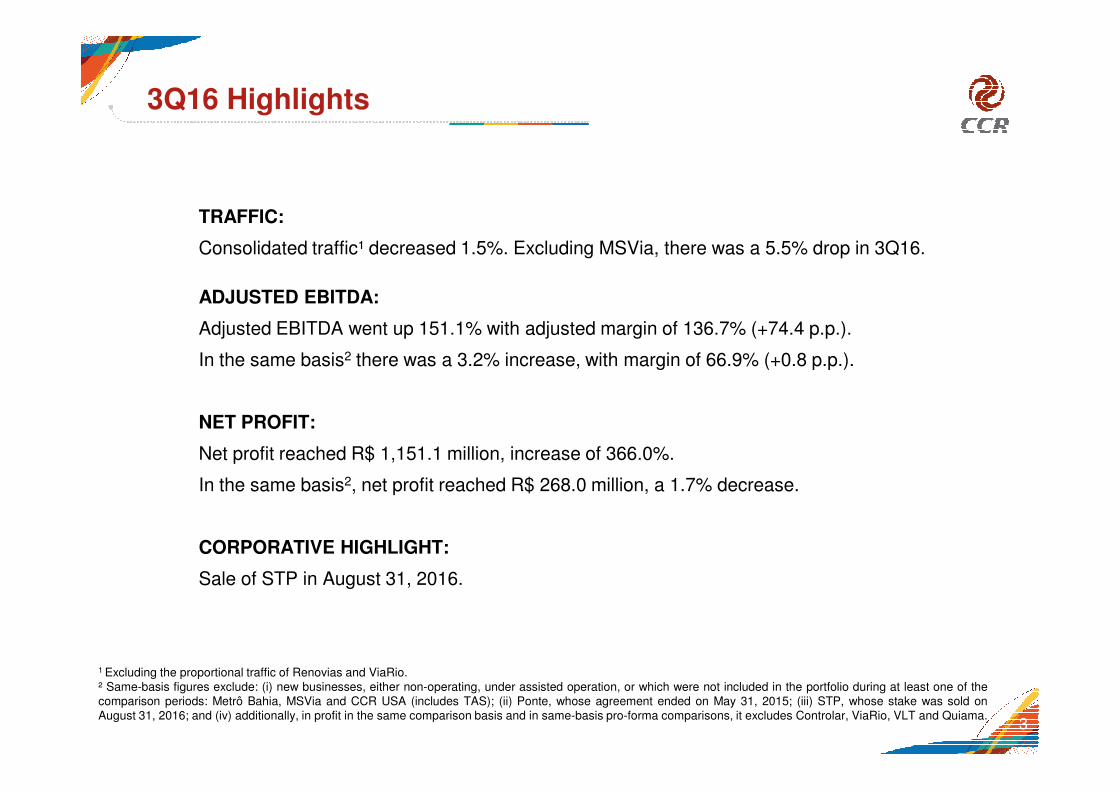

TRAFFIC:

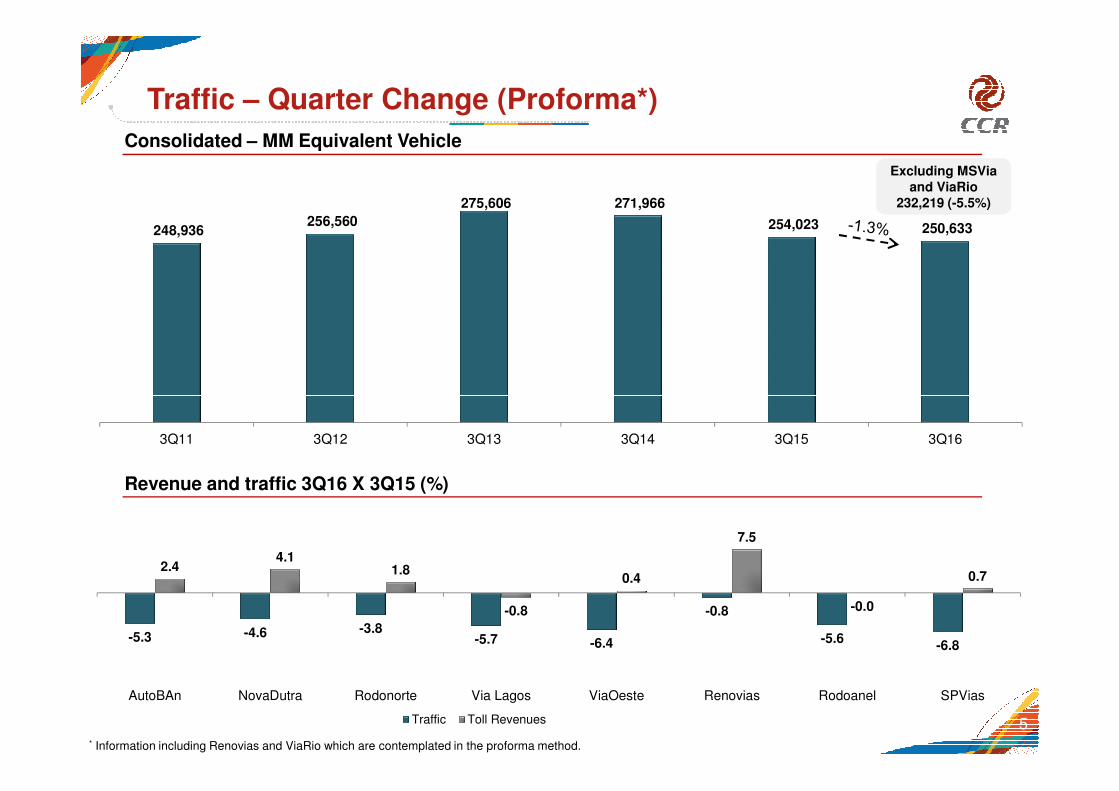

Consolidated traffic¹ decreased 1.5%. Excluding MSVia, there was a 5.5% drop in 3Q16.

ADJUSTED EBITDA:

Adjusted EBITDA went up 151.1% with adjusted margin of 136.7% (+74.4 p.p.).

In the same basis2 there was a 3.2% increase, with margin of 66.9% (+0.8 p.p.).

3Q16 Highlights

NET PROFIT:

Net profit reached R$ 1,151.1 million, increase of 366.0%.

In the same basis2, net profit reached R$ 268.0 million, a 1.7% decrease.

CORPORATIVE HIGHLIGHT:

Sale of STP in August 31, 2016.

3

1 Excluding the proportional traffic of Renovias and ViaRio.² Same-basis figures exclude: (i) new businesses, either non-operating, under assisted operation, or which were not included in the portfolio during at least one of thecomparison periods: Metrô Bahia, MSVia and CCR USA (includes TAS); (ii) Ponte, whose agreement ended on May 31, 2015; (iii) STP, whose stake was sold onAugust 31, 2016; and (iv) additionally, in profit in the same comparison basis and in same-basis pro-forma comparisons, it excludes Controlar, ViaRio, VLT and Quiama.

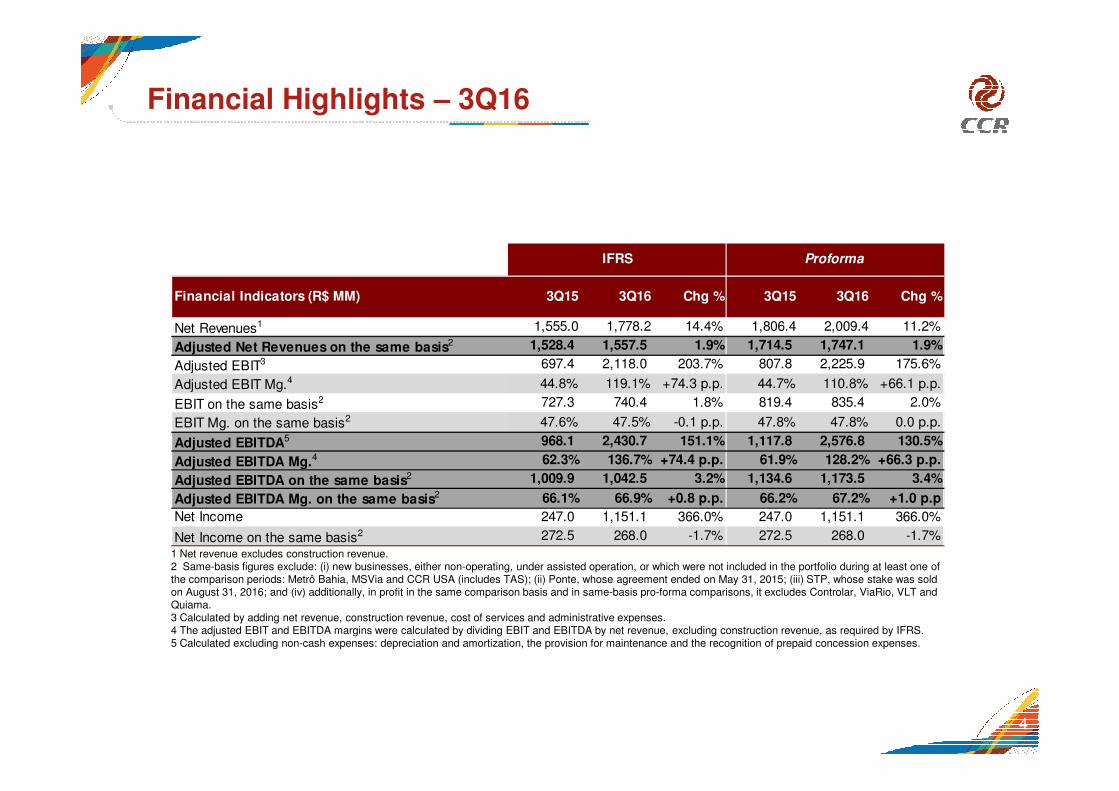

Financial Highlights – 3Q16

Net Revenues1 1,555.0 1,778.2 14.4% 1,806.4 2,009.4 11.2%

Adjusted Net Revenues on the same basis2 1,528.4 1,557.5 1.9% 1,714.5 1,747.1 1.9%

Adjusted EBIT3 697.4 2,118.0 203.7% 807.8 2,225.9 175.6%

Adjusted EBIT Mg.4 44.8% 119.1% +74.3 p.p. 44.7% 110.8% +66.1 p.p.2 727.3 740.4 1.8% 819.4 835.4 2.0%

Proforma

Financial Indicators (R$ MM) 3Q15 3Q16 Chg %

IFRS

3Q15 3Q16 Chg %

1 Net revenue excludes construction revenue.2 Same-basis figures exclude: (i) new businesses, either non-operating, under assisted operation, or which were not included in the portfolio during at least one of the comparison periods: Metrô Bahia, MSVia and CCR USA (includes TAS); (ii) Ponte, whose agreement ended on May 31, 2015; (iii) STP, whose stake was sold on August 31, 2016; and (iv) additionally, in profit in the same comparison basis and in same-basis pro-forma comparisons, it excludes Controlar, ViaRio, VLT and Quiama. 3 Calculated by adding net revenue, construction revenue, cost of services and administrative expenses.4 The adjusted EBIT and EBITDA margins were calculated by dividing EBIT and EBITDA by net revenue, excluding construction revenue, as required by IFRS.5 Calculated excluding non-cash expenses: depreciation and amortization, the provision for maintenance and the recognition of prepaid concession expenses.

4

EBIT on the same basis2 727.3 740.4 1.8% 819.4 835.4 2.0%

EBIT Mg. on the same basis2 47.6% 47.5% -0.1 p.p. 47.8% 47.8% 0.0 p.p.

Adjusted EBITDA5 968.1 2,430.7 151.1% 1,117.8 2,576.8 130.5%

Adjusted EBITDA Mg.4 62.3% 136.7% +74.4 p.p. 61.9% 128.2% +66.3 p.p.

Adjusted EBITDA on the same basis2 1,009.9 1,042.5 3.2% 1,134.6 1,173.5 3.4%

Adjusted EBITDA Mg. on the same basis2 66.1% 66.9% +0.8 p.p. 66.2% 67.2% +1.0 p.p

Net Income 247.0 1,151.1 366.0% 247.0 1,151.1 366.0%

Net Income on the same basis2 272.5 268.0 -1.7% 272.5 268.0 -1.7%

248,936 256,560

275,606 271,966

254,023 250,633

Traffic – Quarter Change (Proforma*)

Consolidated – MM Equivalent Vehicle

Excluding MSViaand ViaRio

232,219 (-5.5%)

3Q11 3Q12 3Q13 3Q14 3Q15 3Q16

5

Revenue and traffic 3Q16 X 3Q15 (%)

* Information including Renovias and ViaRio which are contemplated in the proforma method.

-5.3 -4.6 -3.8 -5.7 -6.4

-0.8

-5.6 -6.8

2.4 4.1

1.8

-0.8

0.4

7.5

-0.0

0.7

AutoBAn NovaDutra Rodonorte Via Lagos ViaOeste Renovias Rodoanel SPVias

Traffic Toll Revenues

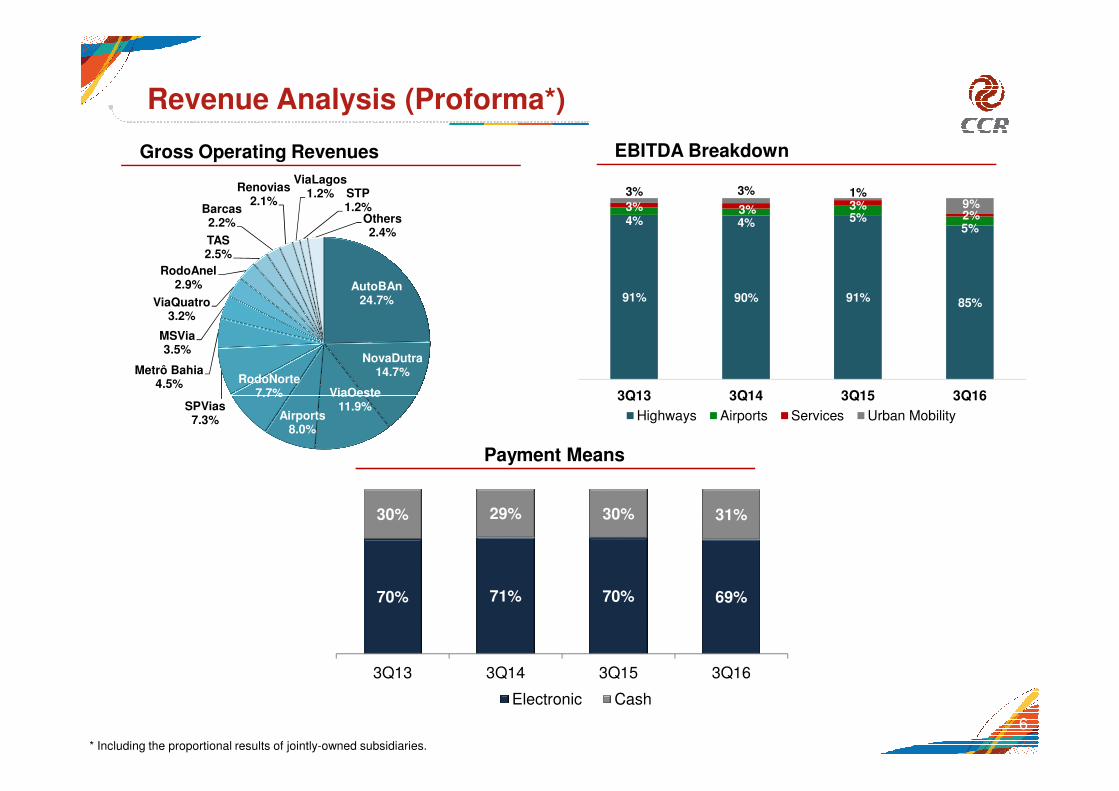

Revenue Analysis (Proforma*)

Gross Operating Revenues EBITDA Breakdown

AutoBAn24.7%

NovaDutra14.7%

ViaOesteRodoNorte

7.7%

Metrô Bahia4.5%

MSVia3.5%

ViaQuatro3.2%

RodoAnel2.9%

TAS2.5%

Barcas2.2%

Renovias2.1%

ViaLagos1.2% STP

1.2%Others2.4%

91% 90% 91% 85%

4% 4% 5%5%

3% 3% 3%2%

3% 3% 1%9%

3Q13 3Q14 3Q15 3Q16

6

Payment Means

* Including the proportional results of jointly-owned subsidiaries.

70% 71% 70% 69%

30% 29% 30% 31%

3Q13 3Q14 3Q15 3Q16

Electronic Cash

ViaOeste11.9%

7.7%

Airports8.0%

SPVias7.3%

3Q13 3Q14 3Q15 3Q16

Highways Airports Services Urban Mobility

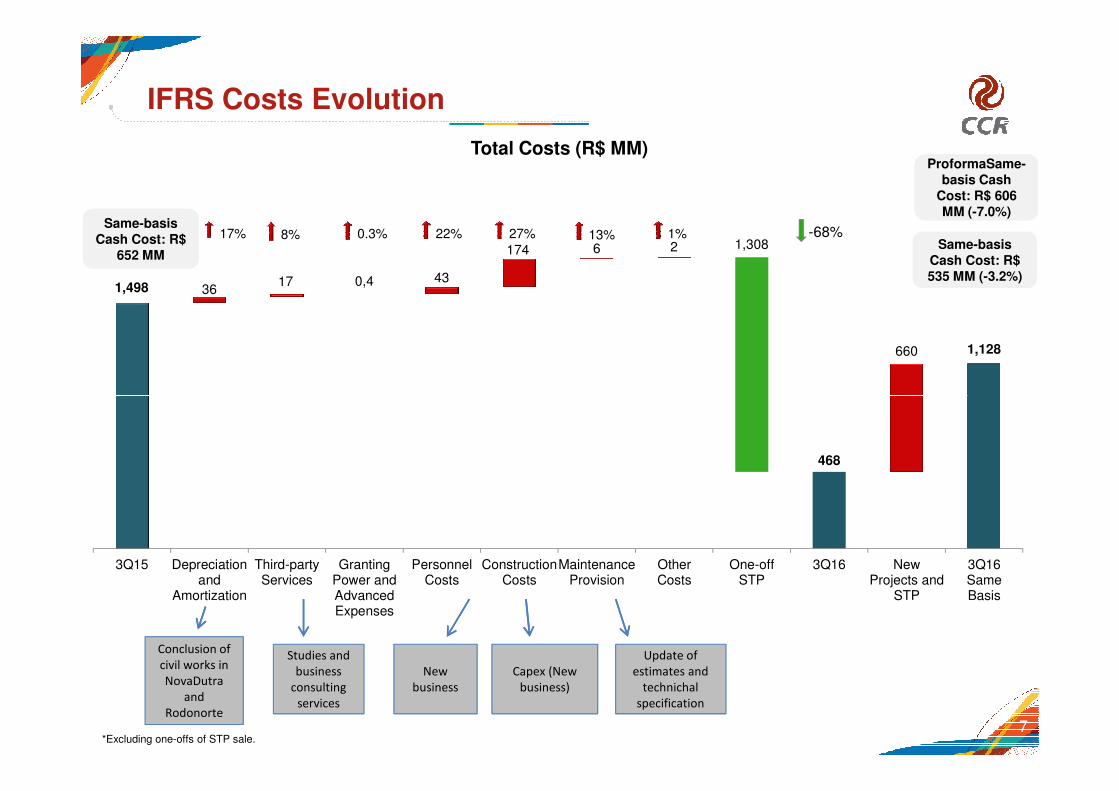

IFRS Costs Evolution

Total Costs (R$ MM)

Same-basis Cash Cost: R$ 535 MM (-3.2%)

8% 22% 27%17% 0.3%Same-basis

Cash Cost: R$ 652 MM

ProformaSame-basis Cash

Cost: R$ 606 MM (-7.0%)

13% 1% -68%

1,498

1,128

3617 0,4 43

174 6 2 1,308

660

7

Conclusion of

civil works in

NovaDutra

and

Rodonorte

Studies and

business

consulting

services

New

business

Capex (New

business)

Update of

estimates and

technichal

specification

*Excluding one-offs of STP sale.

468

3Q15 Depreciationand

Amortization

Third-partyServices

GrantingPower andAdvancedExpenses

PersonnelCosts

ConstructionCosts

MaintenanceProvision

OtherCosts

One-offSTP

3Q16 NewProjects and

STP

3Q16SameBasis

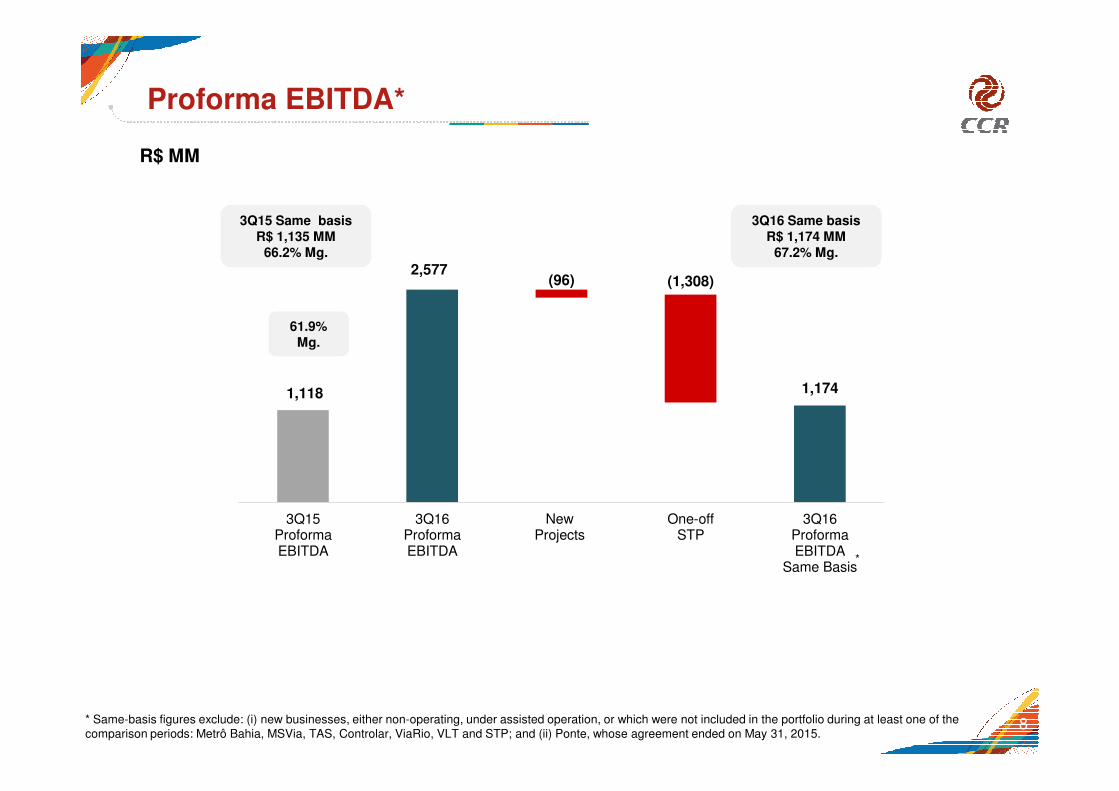

1,118

2,577

1,174

(96) (1,308)

Proforma EBITDA*

61.9%Mg.

3Q15 Same basisR$ 1,135 MM

66.2% Mg.

3Q16 Same basisR$ 1,174 MM

67.2% Mg.

R$ MM

1,118 1,174

3Q15ProformaEBITDA

3Q16ProformaEBITDA

NewProjects

One-offSTP

3Q16ProformaEBITDA

Same Basis

8* Same-basis figures exclude: (i) new businesses, either non-operating, under assisted operation, or which were not included in the portfolio during at least one of the comparison periods: Metrô Bahia, MSVia, TAS, Controlar, ViaRio, VLT and STP; and (ii) Ponte, whose agreement ended on May 31, 2015.

*

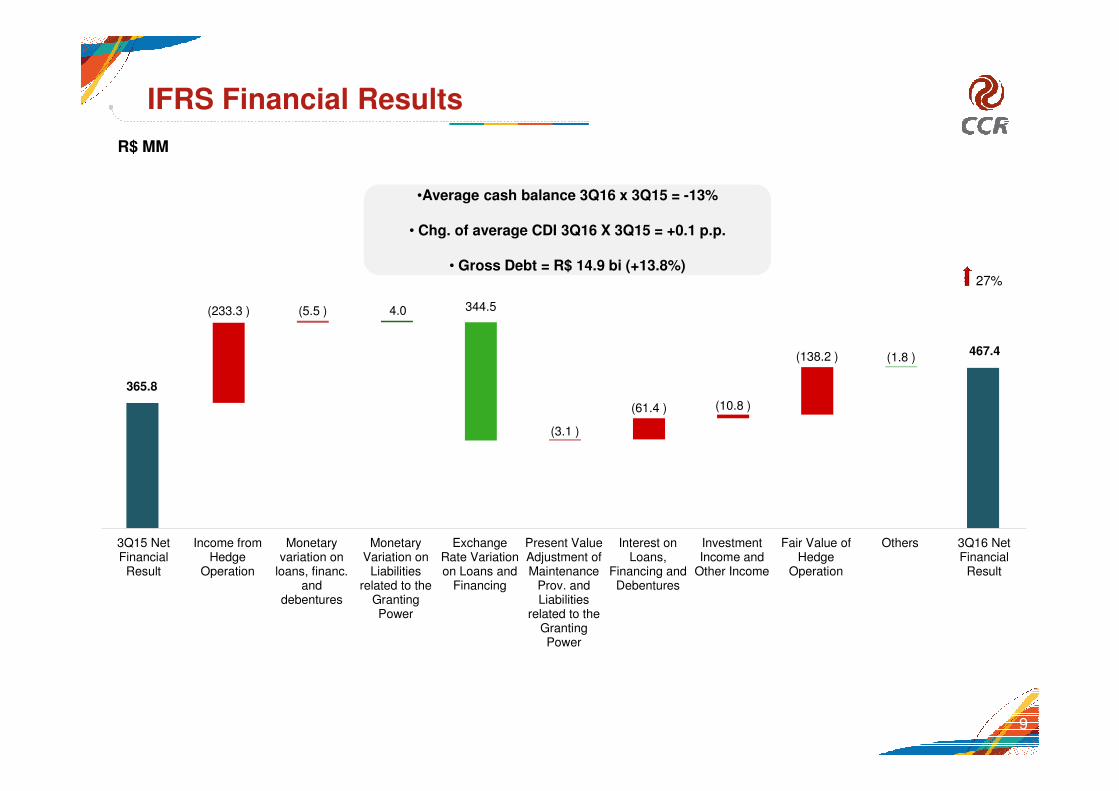

IFRS Financial Results

•Average cash balance 3Q16 x 3Q15 = -13%

• Chg. of average CDI 3Q16 X 3Q15 = +0.1 p.p.

• Gross Debt = R$ 14.9 bi (+13.8%)27%

R$ MM

365.8

467.4

(233.3 ) (5.5 ) 4.0 344.5

(138.2 ) (1.8 )

9

(3.1 )

(61.4 ) (10.8 )

3Q15 NetFinancial

Result

Income fromHedge

Operation

Monetaryvariation on

loans, financ.and

debentures

MonetaryVariation on

Liabilitiesrelated to the

GrantingPower

ExchangeRate Variationon Loans and

Financing

Present ValueAdjustment ofMaintenance

Prov. andLiabilities

related to theGrantingPower

Interest onLoans,

Financing andDebentures

InvestmentIncome and

Other Income

Fair Value ofHedge

Operation

Others 3Q16 NetFinancial

Result

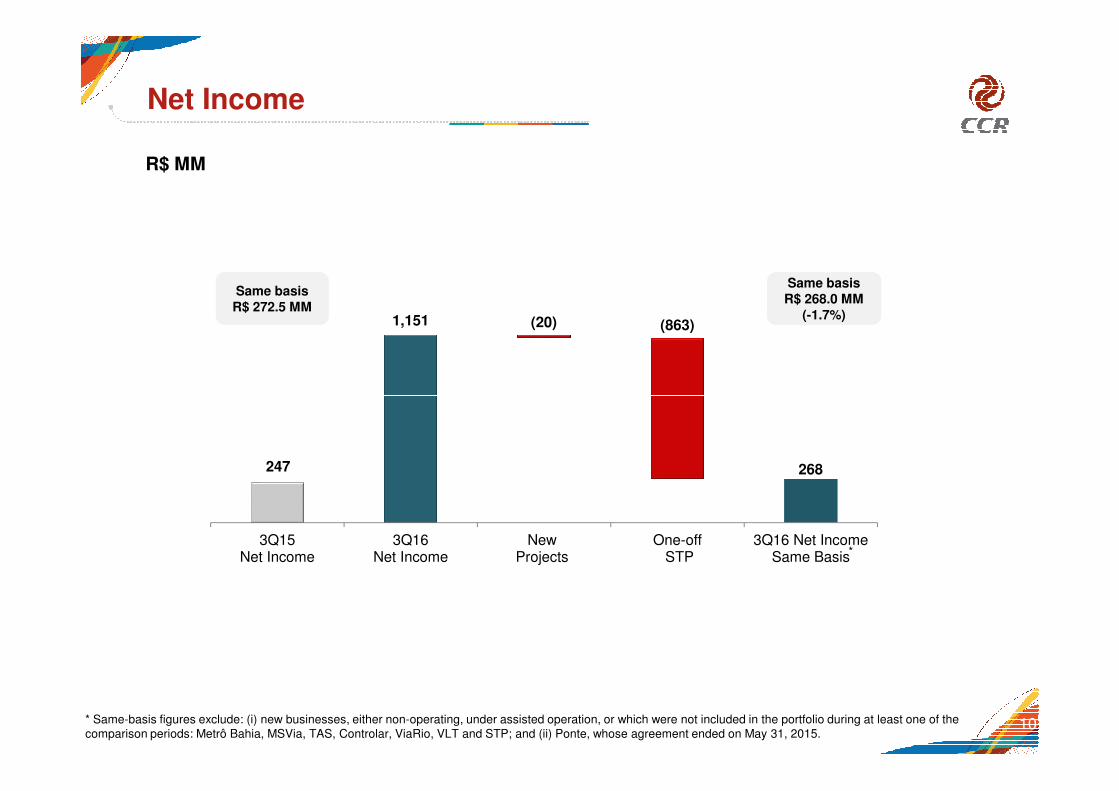

Net Income

R$ MM

Same basisR$ 272.5 MM

Same basisR$ 268.0 MM

(-1.7%)1,151 (20) (863)

10

*

* Same-basis figures exclude: (i) new businesses, either non-operating, under assisted operation, or which were not included in the portfolio during at least one of the comparison periods: Metrô Bahia, MSVia, TAS, Controlar, ViaRio, VLT and STP; and (ii) Ponte, whose agreement ended on May 31, 2015.

247 268

3Q15Net Income

3Q16Net Income

NewProjects

One-off STP

3Q16 Net IncomeSame Basis

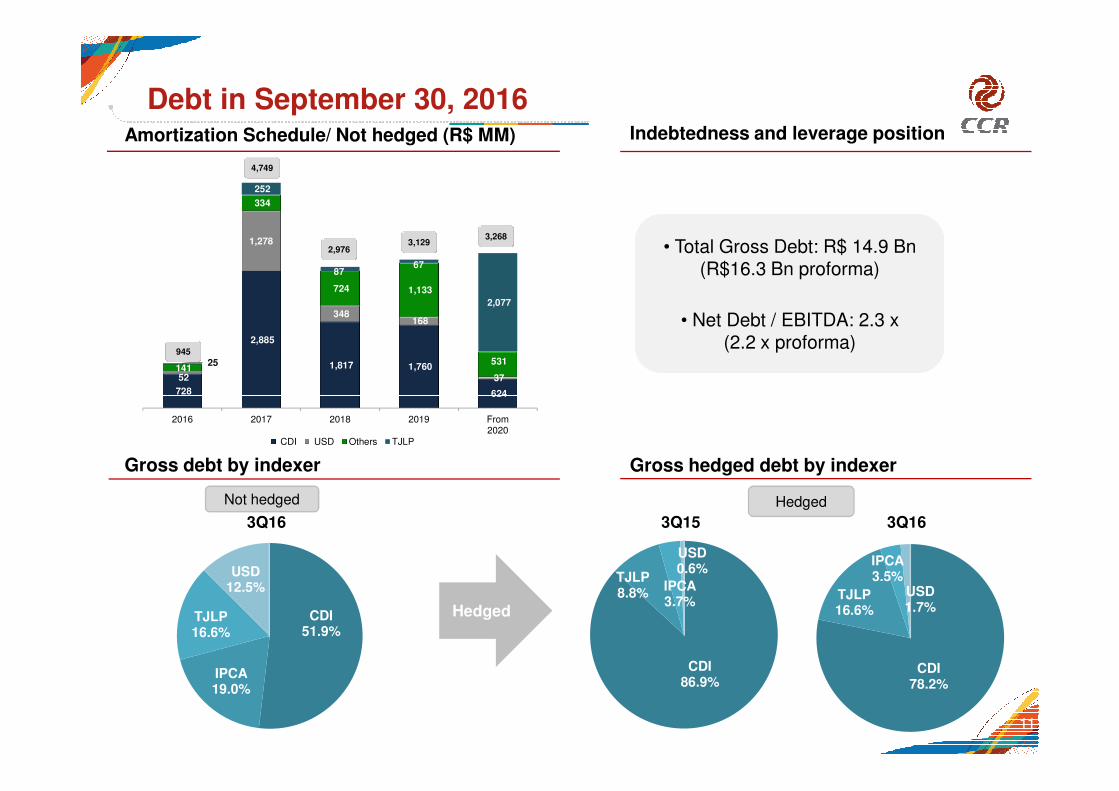

Debt in September 30, 2016Amortization Schedule/ Not hedged (R$ MM) Indebtedness and leverage position

• Total Gross Debt: R$ 14.9 Bn(R$16.3 Bn proforma)

• Net Debt / EBITDA: 2.3 x(2.2 x proforma)

728

2,885

1,817 1,760

624

52

1,278

348 168

37 141

334

724 1,133

531 25

252

87 67

2,077

3,2683,129

2,976

4,749

945

Gross hedged debt by indexer

11

Gross debt by indexer

Not hedged Hedged

HedgedCDI51.9%

IPCA19.0%

TJLP16.6%

USD12.5%

CDI86.9%

TJLP8.8%

IPCA3.7%

USD0.6%

CDI78.2%

TJLP16.6%

IPCA3.5%

USD1.7%

3Q16 3Q163Q15

728 624

2016 2017 2018 2019 From2020

CDI USD Others TJLP

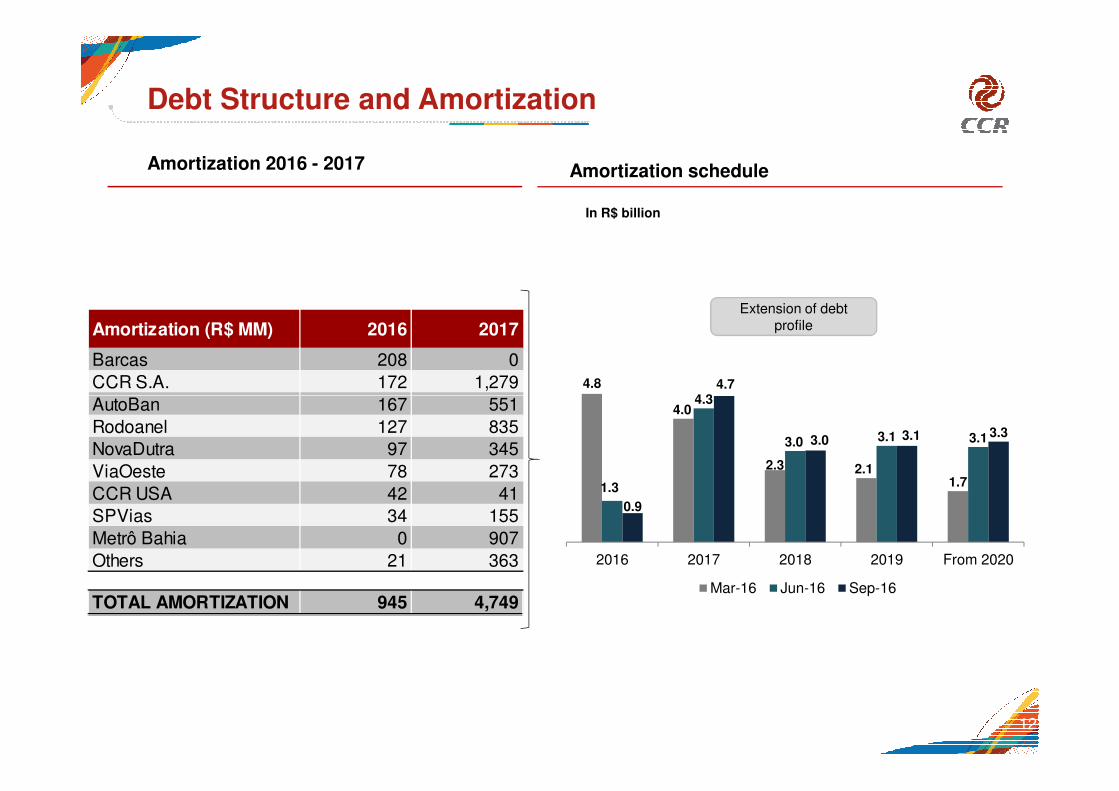

Debt Structure and Amortization

Amortization 2016 - 2017 Amortization schedule

In R$ billion

Extension of debt profileAmortization (R$ MM) 2016 2017

Barcas 208 0

CCR S.A. 172 1,279

AutoBan 167 551

4.84.3

4.7

12

AutoBan 167 551

Rodoanel 127 835

NovaDutra 97 345

ViaOeste 78 273

CCR USA 42 41

SPVias 34 155

Metrô Bahia 0 907

Others 21 363

TOTAL AMORTIZATION 945 4,749

4.0

2.3 2.11.71.3

4.3

3.0 3.1 3.1

0.9

3.0 3.1 3.3

2016 2017 2018 2019 From 2020

Mar-16 Jun-16 Sep-16

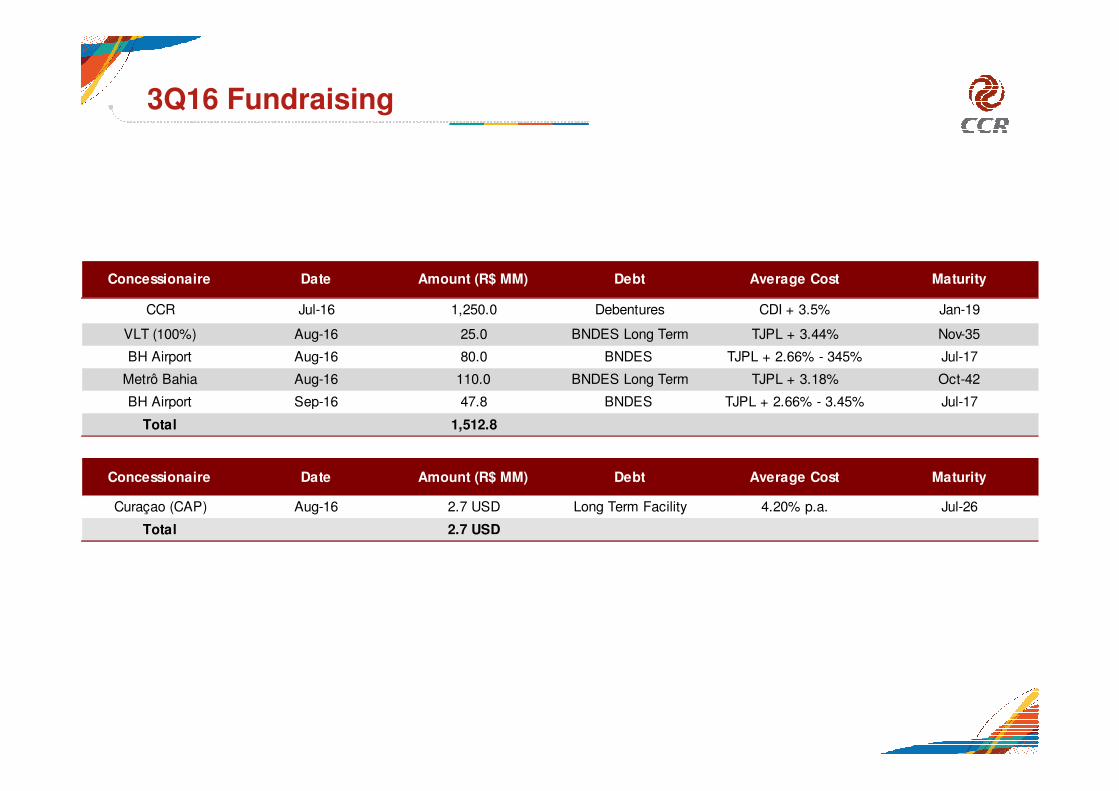

3Q16 Fundraising

Concessionaire Date Amount (R$ MM) Debt Average Cost Maturity

CCR Jul-16 1,250.0 Debentures CDI + 3.5% Jan-19

VLT (100%) Aug-16 25.0 BNDES Long Term TJPL + 3.44% Nov-35

BH Airport Aug-16 80.0 BNDES TJPL + 2.66% - 345% Jul-17

Metrô Bahia Aug-16 110.0 BNDES Long Term TJPL + 3.18% Oct-42

BH Airport Sep-16 47.8 BNDES TJPL + 2.66% - 3.45% Jul-17BH Airport Sep-16 47.8 BNDES TJPL + 2.66% - 3.45% Jul-17

Total 1,512.8

Concessionaire Date Amount (R$ MM) Debt Average Cost Maturity

Curaçao (CAP) Aug-16 2.7 USD Long Term Facility 4.20% p.a. Jul-26

Total 2.7 USD

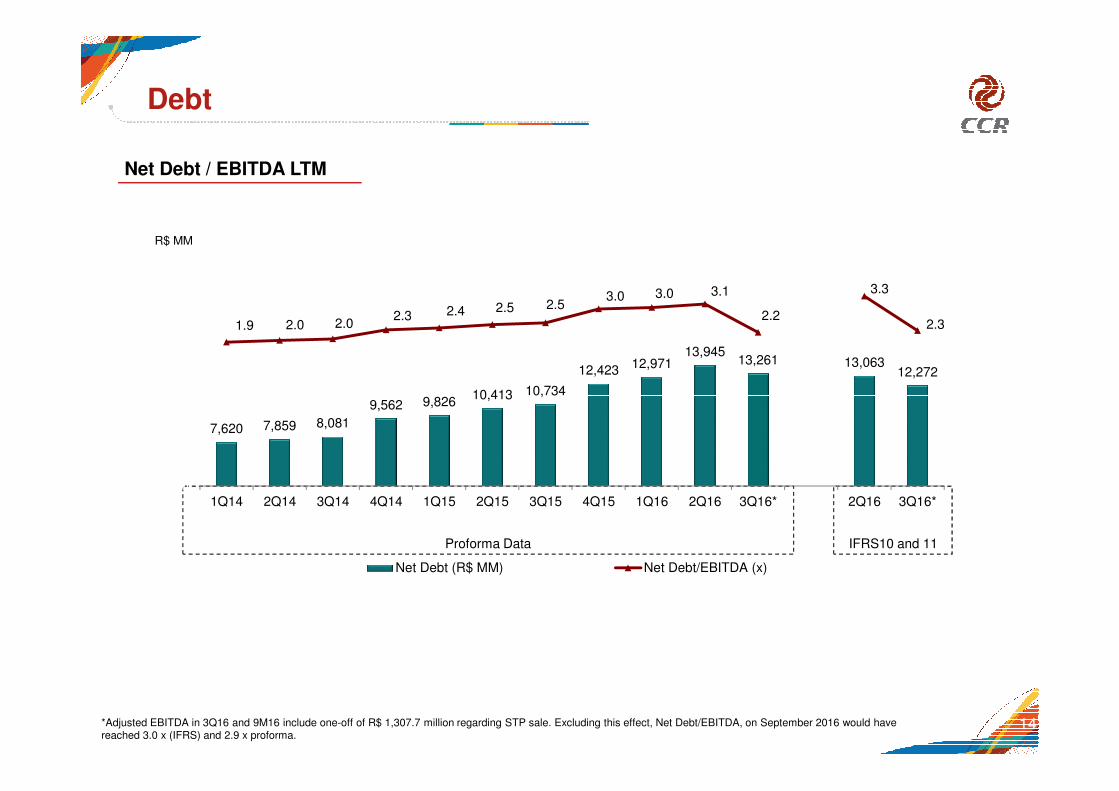

Debt

Net Debt / EBITDA LTM

R$ MM

9,82610,413 10,734

12,423 12,97113,945

13,261 13,06312,272

1.9 2.0 2.02.3 2.4 2.5 2.5

3.0 3.0 3.1

2.2

3.3

2.3

0.5

1.5

2.5

3.5

12,000

14,000

16,000

18,000

20,000

14

IFRS10 and 11Proforma Data

7,620 7,859 8,081

9,562 9,82610,413 10,734

-2.5

-1.5

-0.5

4,000

6,000

8,000

10,000

1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16* 2Q16 3Q16*

Net Debt (R$ MM) Net Debt/EBITDA (x)

*Adjusted EBITDA in 3Q16 and 9M16 include one-off of R$ 1,307.7 million regarding STP sale. Excluding this effect, Net Debt/EBITDA, on September 2016 would have reached 3.0 x (IFRS) and 2.9 x proforma.

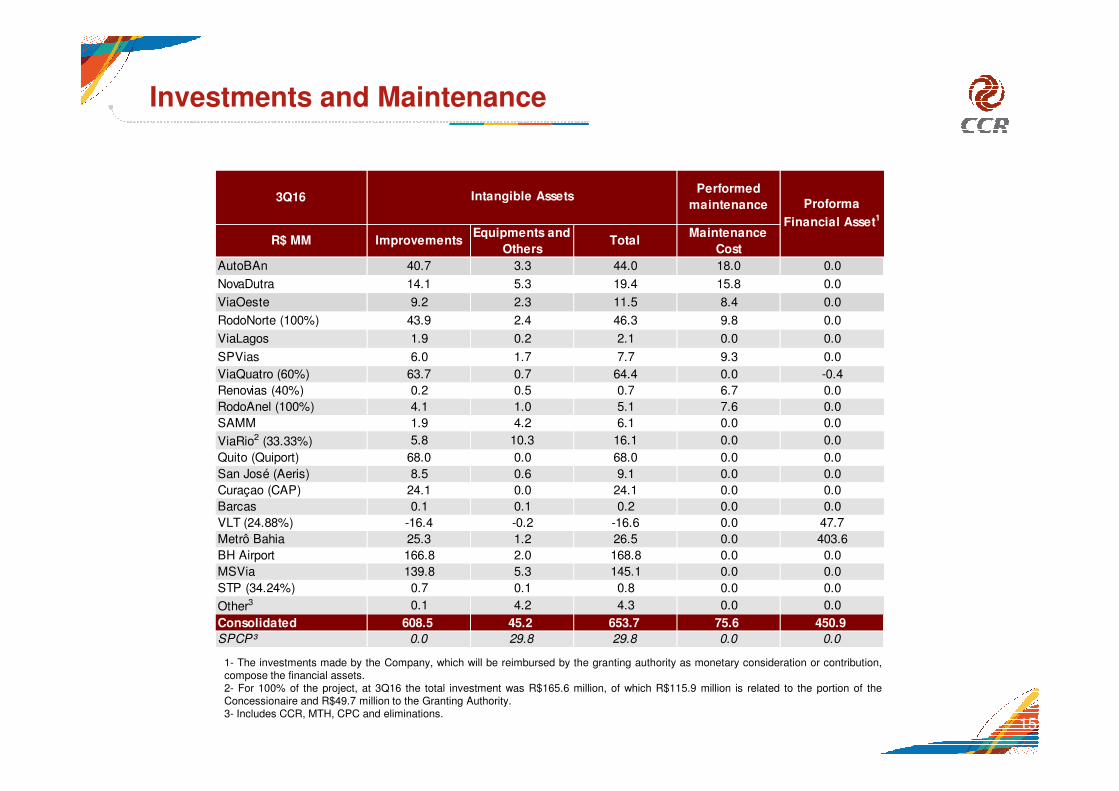

Investments and Maintenance

3Q16

AutoBAn 40.7 3.3 44.0 18.0 0.0

NovaDutra 14.1 5.3 19.4 15.8 0.0

ViaOeste 9.2 2.3 11.5 8.4 0.0

RodoNorte (100%) 43.9 2.4 46.3 9.8 0.0

ViaLagos 1.9 0.2 2.1 0.0 0.0

SPVias 6.0 1.7 7.7 9.3 0.0

ViaQuatro (60%) 63.7 0.7 64.4 0.0 -0.4

Renovias (40%) 0.2 0.5 0.7 6.7 0.0

R$ MM

Proforma

Financial Asset1

ImprovementsEquipments and

OthersTotal

Maintenance

Cost

Intangible AssetsPerformed

maintenance

15

1- The investments made by the Company, which will be reimbursed by the granting authority as monetary consideration or contribution,compose the financial assets.2- For 100% of the project, at 3Q16 the total investment was R$165.6 million, of which R$115.9 million is related to the portion of theConcessionaire and R$49.7 million to the Granting Authority.3- Includes CCR, MTH, CPC and eliminations.

Renovias (40%) 0.2 0.5 0.7 6.7 0.0

RodoAnel (100%) 4.1 1.0 5.1 7.6 0.0

SAMM 1.9 4.2 6.1 0.0 0.0

ViaRio2 (33.33%) 5.8 10.3 16.1 0.0 0.0

Quito (Quiport) 68.0 0.0 68.0 0.0 0.0

San José (Aeris) 8.5 0.6 9.1 0.0 0.0

Curaçao (CAP) 24.1 0.0 24.1 0.0 0.0

Barcas 0.1 0.1 0.2 0.0 0.0

VLT (24.88%) -16.4 -0.2 -16.6 0.0 47.7

Metrô Bahia 25.3 1.2 26.5 0.0 403.6

BH Airport 166.8 2.0 168.8 0.0 0.0

MSVia 139.8 5.3 145.1 0.0 0.0

STP (34.24%) 0.7 0.1 0.8 0.0 0.0

Other3 0.1 4.2 4.3 0.0 0.0

Consolidated 608.5 45.2 653.7 75.6 450.9

SPCP³ 0.0 29.8 29.8 0.0 0.0